9.4 Ethical Issues in the Provision of Health Care

9.4 Ethical Issues in the Provision of Health Care

Learning Objectives

By the end of this section, you will be able to:

Identify ethical problems related to the availability and cost of health care in the United States and elsewhere

Discuss recent developments in insuring or otherwise providing for health care in the United States

Private health care in the United States has historically been of high quality and readily available, but only for those who could afford it. This model for rationing health services is rare in the developed world and stands in dramatic contrast to the provision of health care in other industrialized economies. Those who provide health care and administer the health care system find that balancing the quality of, access to, and cost of medical care is an ethical dilemma in which they must continually engage.30

Multipayer Health Care in the United States

Typically in the United States, medical services have been dispensed through a multipayer health care system, in which the patient and others, such as an employer and a private health insurance company, all contribute to pay for the patient’s care. Germany, France, and Japan also have multipayer systems. In a single-payer health care system such as those in the United Kingdom and Canada, national tax revenues pay the largest portion of citizens’ medical care, and the government is the sole payer compensating those who provide that care. Contributions provided by employers and employees provide the rest. Both single- and multipayer systems help reduce costs for patients, employers, and insurers; both, especially single-payer, are also heavily dependent on taxes apportioned across employers and the country’s population. In a single-payer system, however, because payment for health care is coordinated and dispensed by the government, almost no one lacks access to medical services, including visitors and nonpermanent residents.

Many reasons exist for the predominance of the multipayer system in the United States. Chief among these is the U.S. tradition that doctors’ services and hospital care are privatized and run for profit. The United States has no federal health care apparatus that organizes physicians, clinics, and medical centers under a single government umbrella. Along with the profit motive, the fact that providers are compensated at a higher average rate than their peers abroad ensures that health care is more expensive in the United States than in most other nations.

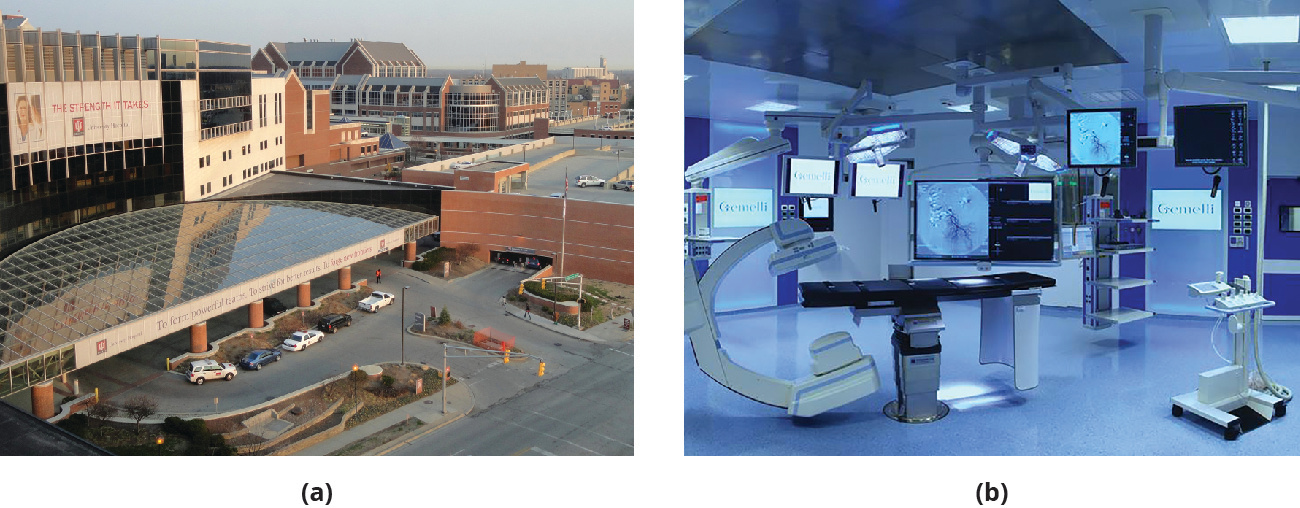

The United States also has more health care professionals per citizen than most other countries, and more medical centers and clinics (Figure 9.5). One positive result is that the wait for most elective medical procedures is often shorter than in other countries, and travel time to a nearby medical facility is often less. Still, paying for health care remains one of the most controversial topics in the United States, and many question what it is that Americans gain from the current system to balance the cost. As an exhaustive study from The Commonwealth Fund asserted, “the United States spends far more on health care than other high-income countries, with spending levels that rose continuously over the past three decades. . . . Yet the U.S. population has poorer health than other countries.”31

Figure 9.5 The Indiana University Health University Hospital (a) is an example of a contemporary medical center affiliated with a university medical school, in this case on the Indiana University–Purdue University Indianapolis campus. This is indicative of a common partnership through which hospitalization and medical-school education are made available in the United States. This type of affiliation also exists abroad, as evidenced by this state-of-the-art operating facility (b) at the Gemelli University Hospital in Rome, Italy. (credit a: modification of “Indiana University Hospital – IUPUI – DSC00508” by “Daderot”/Wikimedia Commons, Public Domain; credit b: modification of “Hybrid operating room for cardiovascular surgery at Gemelli Hospital in Rome” by “Pfree2014”/Wikimedia Commons, CC0)

Besides its inefficiencies, the state of U.S. health care raises challenging ethical issues for professionals in the field and for patients as well. What happens if many poorer people cannot afford health care? Should doctors treat them anyway? Who is qualified to receive subsidized (insured) health care? In the absence of universal health care, which is generally ensured elsewhere by a single-payer system that entitles everyone to receive care at very low cost, can the United States truly boast of being the richest nation on Earth? Put another way, when the least materially advantaged in a country do not have access to quality health care, what is the worth such a nation patently is assigning to those human beings residing within it?

Supporters of the status quo for health care in the United States may point to state-of-the-art facilities as evidence of its success. Yet other nations, such as Australia, the United Kingdom, and the Netherlands, have equal levels of medical technologies available for patients and are given much more favorable marks for universal health insurance and accessibility by The Commonwealth Fund.

The High Cost of Prescription Drugs

Discussions of health care accessibility have become politically charged, so for now it is enough to observe that not only is medical care enormously expensive in the United States but so are prescription drugs. According to William B. Schultz, an attorney writing in the Washington Post in 2017, “in the past 35 years, the only significant victory in the battle to control drug prices has been the enactment of legislation that established the generic drug program at the FDA [Federal Drug Administration].” Otherwise, he stated, “prescription drug prices account for 17 percent of the nation’s health-care costs, up from 7 percent in the 1990s,” and “prescription drug spending accounts for nearly 20 percent of total program spending for Medicare, the largest of the governmental health-care programs.”32 (Schultz is not entirely impartial; he is a partner in a law firm that represents generic drug providers, among other clients.)

Link to Learning

The New York Times asked its readers to relay their experiences as purchasers of prescribed medicines that they thought carried much too high a price tag. This article on some of the reader responses to drug prices was reported by two journalists at the paper, Katie Thomas and Charles Ornstein.

The only way to recoup the enormous cost of developing new drugs, says the pharmaceutical industry, is to pass it along to consumers. Critics, on the other hand, assert that the much of the expense incurred within the industry results from the high cost of marketing new drugs. Wherever the truth lies in this debate, it remains that exorbitant prices for much-needed medicines dramatically reduce their social value when only a few individuals can actually afford to obtain them. What does it say of our priorities if we have the technology to create life-saving medicines but allow astronomic prices effectively to deny them to many patients who require them?

Paying for Health Care and Wellness

Within the multipayer system, many U.S. workers have traditionally looked to their employers or their unions to subsidize the cost of care and thereby make it available for them and their families. Many reasons explain why this is so. In contrast to the European and Canadian perspective, for example, in which both the state and employers are presumed to have an interest in and responsibility for underwriting the cost of health care, the traditional U.S. approach is that workers and their employers should be responsible for securing this coverage. This belief reflects an unease on the part of some about assigning services to the government, because this implies the need for a larger governing entity as well as additional taxes to sustain it. The sentiment also reflects a conviction on the part of some that self-reliance is always to be preferred when securing the necessities of life.

John E. Murray, a professor of economics at the University of Toledo, offered a related explanation. He cited the existence of industrial sickness funds in the United States, which arose in the late nineteenth and early twentieth centuries. These were monies “organized by workers through their employer or union [that] provided the rudiments of health insurance, principally consisting of paid sick leave, to a large minority of the industrial workforce of the late nineteenth and early twentieth centuries.”33 Murray stated that these funds declined in popularity not because they were ineptly administered or rendered bankrupt by World War I or the Great Depression but rather because they gave way to even more effective instruments in the form of group insurance policies offered by employers or labor unions.

So the U.S. worker’s experience differed from that of European labor in that much significant health care coverage was provided under the auspices of unions and employers rather than the state. Murray noted another source of relief for workers who experienced illness or injury that prevented them from working for any period of time, and that was charity.34 Specific versions of charity were offered by religious organizations, including Christian churches and Jewish synagogues. Often, these religious bodies banded together to provide monetary benefits for sick or injured members of their own faith who might otherwise have been denied health coverage due to prejudice.35 The U.S. social experience featured more ethnic and cultural diversity, especially in the nineteenth and early twentieth centuries, than was present in many European nations, and a downside is the racial, ethnic, and religious prejudice it inspired.

A final distinction Murray pointed to is the past opposition of the American Medical Association to any sort of state-sponsored insurance. Early supporters of industrial sickness funds, including some physicians, anticipated that most doctors would support these funds as pathways ultimately directed to state-provided coverage. Instead, in 1920, “the American Medical Association voted officially to state its opposition to government health insurance. A sociologist concluded that from this time to the 1960s, physicians were the loudest opponents of government insurance.”36 By default, then, many U.S. workers came to rely more on their employers or unions than on any other source for coverage. However, this explanation does not answer the larger ethical question of who should provide health insurance to residents and citizens, a question that continues to roil politics and society in the nation even today.

Physicians and other healthcare professionals in the United States have always been held to high ethical standards in terms of the care they provide their patients. In fact, the American Medical Association first proposed a code of medical ethics in 1847, its founding year. Since then, the AMA has continued to revisit precisely what constitutes medical ethics for its members. In 2008, its code of medical ethics was revised.37 The revisions imply that education in medical ethics for healthcare professionals is not accomplished once and for all. Rather, retraining and recertification is an ongoing process.

More recently, large corporations have moved from providing one-size-fits-all insurance plans to compiling a menu of offerings to accommodate the different needs of their employees. Workers with dependent children may opt for maximum health care coverage for their children. Employees without dependents or a partner may elect a plan without this coverage and thereby pay lower premiums (the initial cost for coverage). Yet others might minimize their health-insurance coverage and convert some of the employer costs that are freed up into added pension or retirement plan value. Employers and workers have become creative in tailoring benefit plans that best suit the needs of employees (Figure 9.6). Some standard features of such plans are the copayment, a set fee per service paid by the patient and typically negotiated between the insurance carrier and the employer; the annual deductible, a preset minimum cost for health care for which the patient is responsible each year before the carrier will assume subsequent costs; and percent totals for certain medical or dental procedures that patients must pay before the carrier picks up the remainder.

Figure 9.6 Anthem Inc. (formerly WellPoint, Inc.), headquartered in Indianapolis, Indiana, is one of the largest health care vendors in the nation, with more than fifty thousand employees and nearly $2.5 billion in net revenue in fiscal year 2016. (credit: modification of “Company headquarters on Monument Circle in Indianapolis” by Serge Melki/Wikimedia Commons, CC BY 2.0)

Despite the intricacies of this customization, employers have found the group coverage policies they offer to be expensive for them too, more so with each passing year. Full health care coverage is becoming rarer as a standard employment benefit, and it is often available only to those who work full time. California, for example, stipulates that most workers need not be provided with employer health care coverage unless they work at least twenty hours a week.

Rising costs for both employers and employees have combined to leave fewer employees with health care benefits at any given time. Employees with limited or no coverage for themselves and their dependents often cope by cutting back on the medical attention they seek, even when doing so places their health at risk. Whenever workers must skip medical services due to cost considerations, this places both them and their employers in an ethical quandary, because both typically want workers to be in good health. Furthermore, when employees must deny their dependents appropriate health care, this dilemma is all the more intensified.

To try to reduce the costs to themselves of employee health care insurance coverage, some companies have instituted wellness programs to try to ensure that their workforces are as healthy as possible. Some popular wellness program offerings are measures to help smokers quit, workout rooms on work premises or subsidized gym memberships, and revamped vending and cafeteria offerings that provide a range of healthier choices. Some companies even offer employees bonuses or other rewards for quitting smoking or achieving specific fitness goals such as weight loss or miles walked per week. Such employer efforts appear benign at first glance, because these measures truly can produce better health on the part of workers. Still, ethical questions arise as to who the true beneficiaries of such policies are. Is it the employees themselves or the companies for which they work? Furthermore, if such measures were to become compulsory rather than optional, would it still reflect managerial benevolence toward employees? We discuss this in the following paragraphs.

Wellness programs were inspired by safety programs first created by U.S. manufacturers in the 1960s. These companies included Chrysler, DuPont, and Steelcase. Safety programs were intended to reduce workplace accidents resulting in injuries and deaths. Over the years, such programs slowly but steadily grew in scope to encompass the general health of employees on the job. As these policies have expanded, they also have fostered some skepticism and resistance: “Wellness programs have attracted their share of criticism. Some critics argue workplace programs cross the line into employees’ personal lives.”38 Ann Mirabito, a marketing professor at the Hankamer School of Business at Baylor University agrees there is potential for abuse: “It comes back to the corporate leader. . . . The best companies respect employees’ dignity and offer programs that help employees achieve their personal goals.”39

Employees who exercise, eat healthily, maintain their ideal weight, abstain from smoking, and limit their alcoholic consumption have a much better chance of remaining well than do their peers who undertake none of these activities. The participating employees benefit, of course, and so do their employers, because the health insurance they provide grows cheaper as their workers draw on it less. As Michael Hiltzik, a consumer affairs columnist for the Los Angeles Times, noted, “Smoking-cessation, weight-loss and disease-screening programs give workers the impression that their employers really care about their health. Ostensibly they save money too, since a healthy workforce is cheaper to cover and less prone to absenteeism.”40

Certainly, employers are also serving their own interests by trying to reduce the cost of insuring their workers. But are there any actual disadvantages for employees of such wellness programs that employers might unethically exploit? Hiltzik suggested one: “The dark downside is that ‘voluntary’ wellness programs also give employers a window into their workers’ health profiles that is otherwise an illegal invasion of their privacy.”41 Thus the health histories of workers become more transparent to their bosses, and, Hiltzik and others worry, this previously confidential information could allow managers to act with bias (in employee evaluation and promotion decisions, for instance) under cover of concern about employees’ health.

The potential for intrusion into employee privacy through wellness programs is alarming; further, the chance for personal health data to become public as a consequence of enrolling in such programs is concerning. Additionally, what about wellness rules that extend to workers’ behavior off the job? Is it ethical for a company to assert the right to restrict the actions of its employees when they are not on the clock? Some, such as researchers Richard J. Herzog, Katie Counts McClain, and Kymberleigh R. Rigard, argue that workers surrender a degree of privacy simply by going onto payroll: “When employees enter the workplace, they forfeit external privacy. For example, BMI [body mass index] can be visually calculated, smokers can be observed, and food intake monitored.” They acknowledge, however, that “protecting privacy and enhancing productivity can provide a delicate balance.”42

Link to Learning

As noted in previous chapters, we can find out a great deal about the ethical intentions of a company by studying its mission statement, although even the noblest statement is irrelevant if the firm fails to live up to it. Here is Anthem, Inc.’s very simple and direct mission statement as an example from a health care insurer. What impression does this statement leave with you? Would you add or delete anything to it? Why or why not?

The Affordable Care Act

Health care reform on a major scale emerged in the United States with the passage of the Patient Protection and Affordable Care Act, more commonly known as the Affordable Care Act (ACA), in March 2010, during the Obama Administration. The ACA (so-called Obamacare) represents a controversial plan that strikes its opponents as socialist. For its supporters, however, it is the first effective and comprehensive plan to extend affordable health care to the widest segment of the U.S. population. Furthermore, like most new federal policies, it has undergone tweaks and revision each year since becoming law. The ACA is funded by a combination of payments by enrollees and supplemental federal monies earmarked for this task.

The ACA mandates a certain level of preventive care, a choice of physicians and health care facilities, coverage at no extra cost for individuals with preexisting health conditions, protection against the cancellation of coverage solely on the basis of becoming ill, and mental health and substance abuse treatment, all of which must be met by carriers that participate in the plan. The ACA also permits its holders to select from a number of marketplace plans as opposed to the limited number of plans typically offered by any given employer.43 All in all, it is a far-reaching and complex plan whose full implications for employers and their employees have yet to be appreciated. Preliminary results seem to indicate that employer-provided coverage on a comprehensive scale remains a cheaper alternative for those workers eligible to receive it.44 Given the general efficiency of group insurance policies provided by U.S. employers, an ethical issue for all managers is whether these policies offer the best care for the greatest number of employees and so should be the responsibility of management to offer whenever it is possible to do so. Current law requires all companies employing fifty or more workers to make insurance available to that part of their workforce that qualifies for such coverage (e.g., by virtue of hours worked). Is it right, however, to leave the employees of smaller firms to their own devices in securing health care? Even if the law does not require it, we hold that an ethical obligation resides with small businesses to do everything in their power to provide this coverage for their employees.

Evidence of the intense debate the act has engendered is the Trump administration’s attempts, beginning in January 2017, to repeal the ACA entirely, or at least to dilute significantly many of its provisions. Nearly immediately upon his inauguration, President Trump signed Executive Order 13765 in anticipation of ending the ACA. Also that same month, the American Health Care Act was introduced in the House of Representatives, again with an eye to eliminating or seriously weakening the existing act. Much political debate within both the House and Senate ensued in 2017, with proponents of the ACA seeking to ensure its survival and opponents attempting (but, as of this writing, failing) to repeal it.

The ACA represents the first far-reaching health care coverage to take effect since 1965, after many stalled or otherwise frustrated attempts. Since the passage that year of the Medicare and Medicaid Act, which provided health coverage to retired, elderly, and indigent citizens, many presidential administrations, Democrat and Republican alike, have worked to enlarge health care coverage for different segments of the national population. In addition to expanding eligibility for benefits, the Medicare and Medicaid Act had direct implications for business proprietors and their employees. For one, the act set up new automatic earnings deductions and tax schedules for workers and employers, and employers were made responsible for administering these plans, which help fund the programs’ benefits.

The future of the ACA appears to depend on whether a Democrat or Republican sits in the White House and which party controls the Senate and the House in the U.S. Congress. Although legislation does hinge on the political sentiments of the president and the majority party in Congress, what is ethical does not lend itself to a majority vote. So regardless of whether the ACA survives, is revised, or is replaced entirely by new health care legislation, the provision of health care will likely continue to pose ethical implications for U.S. business and the workers who are employed by it.

The ethical debate over universal health care coverage is larger even than business and its employees, of course, but it still carries immense consequences for management and labor irrespective of how the ACA or other legislation fares in the halls of government and the courts. An ethical dilemma for employers is the extent to which they should make health coverage available to their workers at affordable rates, particularly if federal and state government plans provide little or no coverage for residents and the costs of employer-provided coverage continues to climb.

State-Level Experiments with Single-Payer Health Care Plans

Against the backdrop of federal attempts to institute national health care over the past several decades, some individual states in the United States have used their own resources to advance this issue by proposing mandated health care coverage for their citizens. For example, in April 2006, Massachusetts passed An Act Providing Access to Affordable, Quality, Accountable Heath Care, the first significant effort at the state level to ensure near-universal health care coverage.

The Massachusetts act created a state agency, the Commonwealth Health Insurance Connector Authority, to administer the extension of health care coverage to Massachusetts residents. In many ways, it served as the most significant precursor of and guide for the federal ACA, which would follow approximately four years later. By many accounts, the Massachusetts legislation has achieved its purposes with few negative consequences. As Brian C. Mooney, reporting in the Boston Globe, put it about five years after the act’s passage: “A detailed Globe examination [of the implementation of the act] makes it clear that while there have been some stumbles—and some elements of the effort merit a grade of ‘incomplete’—the overhaul, after five years, worked as well as or better than expected.”45

The proposed Healthy California Act (SB 562) is another example. SB 562 passed in the California State Senate in June 2017. However, the Speaker of the Assembly, the lower house of the legislature, blocked a hearing of the bill at that time, and a hearing is necessary for the bill to advance to ratification. A new effort was initiated in February 2018 to permit the bill finally to be considered by the lower house. (Two differences between the California bill and the Massachusetts Act include the number of state residents who would be affected. Massachusetts has a population of about seven million compared to California’s nearly forty million. A second distinction is that SB 562 is constitutes a single-payer plan, whereas the Massachusetts Act does not.)

Single-payer health care plans essentially concentrate both the administration of and payment for health care within one entity, such as a state agency. California’s effort is a very simple plan on its face but complex in its implementation. Here is how Michael Hiltzik summarized the intent of California Senate Bill 562: “The program would take over responsibility for almost all medical spending in the state, including federal programs such as Medicare and Medicaid, employer-sponsored health plans, and Affordable Care Act plans. It would relieve employers, their workers and buyers in the individual market of premiums, deductibles and copays, paying the costs out of a state fund.”46 The bill would create a large, special program apparatus tentatively entitled Healthy California. It is contentious on many fronts, particularly in that it would create the largest single-payer health insurance plan sponsored by a U.S. state and the scope of the plan would necessitate a huge bureaucracy to administer it as well an infusion of state monies to sustain it. Furthermore, it would extend health care coverage to all residents of the state, including undocumented immigrants.

A specific hurdle to passage of Healthy California is that it would cost anywhere from $370 billion to $400 billion and would require federal waivers so California could assume the administration of Medicare and Medicaid in the state as well as the federal funds currently allotted to it. All these conditions would be enormously difficult and time consuming to meet, even if the federal government were sympathetic to California’s attempts to do so. In 2018, that was decidedly not the case.

Is free or inexpensive access to health care a basic human right? If so, which elements within society bear the principal responsibility for providing it: government, business, workers, all these, or other agencies or individuals? This is a foundational ethical question that would invoke different responses on the part of nearly everyone you may ask.

Ethics Across Time and Cultures

Free Universal Health Care

Except for the United States, the largest advanced economies in the world all provide a heavily subsidized universal health care system, that is, a publicly funded system that provides primary health services to all, usually at a nominal fee only and with no exclusions based on income or wealth. Although these systems are not perfect, their continued existence seems assured, regardless of the cultural or political framework of the various countries. A logical question is why the United States would be an outlier on this issue, and whether that might change in the future.

Some answers, as noted in the text, lie in the United States’ historical reliance on a mostly private system, with approximately 83 percent of health care expenses provided by the private sector through insurers and employers (in contrast, this percentage in the United Kingdom is 17). A solution that has gained traction in recent years is conversion to a single-payer system. How might this work? One article estimates that the cost of instituting a national, single-payer health care insurance program in the United States would be $32 trillion over ten years. If this estimate is accurate, would it be an exorbitant price tag for such a program, or would it be money well spent in terms of making good health care available to all citizens?47

Critical Thinking

Do you find it appropriate that health care costs be provided by a mix of private versus public sources?

What advantages might single-payer health care offer over employer-provided coverage, care provided under the ACA, or privately purchased health insurance?

As a nation, the United States has usually preferred a system predicated on private health care providers and insurers to pay for it. This arrangement has worked best in instituting high-quality care with minimal delays even for elective medical procedures. It has systematically failed, however, in establishing any sort of universal dispensation that is affordable for many citizens.

In the early twenty-first century, the United States is moving ever so slowly and with plenty of hiccups toward some degree of national or state management of health care. Precisely where these efforts will take us may not be clear for the next several years. The political, economic, and ethical dimensions of public management of our health care drive considerable controversy and very little agreement.